Buying or Owning a Laundromat? Essential Escrow Tips Straight From Podcast Episode 241

If you’re considering buying your first laundromat or you already own one, understanding the escrow process is one of the most crucial steps in making sure your investment pays off. In Laundromat Resource Podcast Show 241, Jordan Berry sits down with escrow professional Justin Suh to break down everything future owners and current operators need to know about escrow. Here are the key takeaways, explained with actionable advice to help you navigate your next transaction smoothly.

1. Always Use a Neutral Escrow Company for Business Transactions

Why it Matters:

Escrow companies serve as independent, non-biased third parties responsible for ensuring both buyer and seller uphold the terms of your mutual agreement. They don’t favor either side, but enforce what both parties have signed.

Practical Application:

Never hand deposits or earnest money directly to the owner or broker (Jordan Berry warns about this on 21:08). Instead, send all deposits through the escrow company. This protects your funds; if a deal falls through, you won’t have to chase your money.

When you decide to begin a purchase, make sure the agreement is completely signed by both buyer and seller before escrow is initiated. If you’re selling, gather all legal documents (like your business license) ahead of time to make escrow move faster.

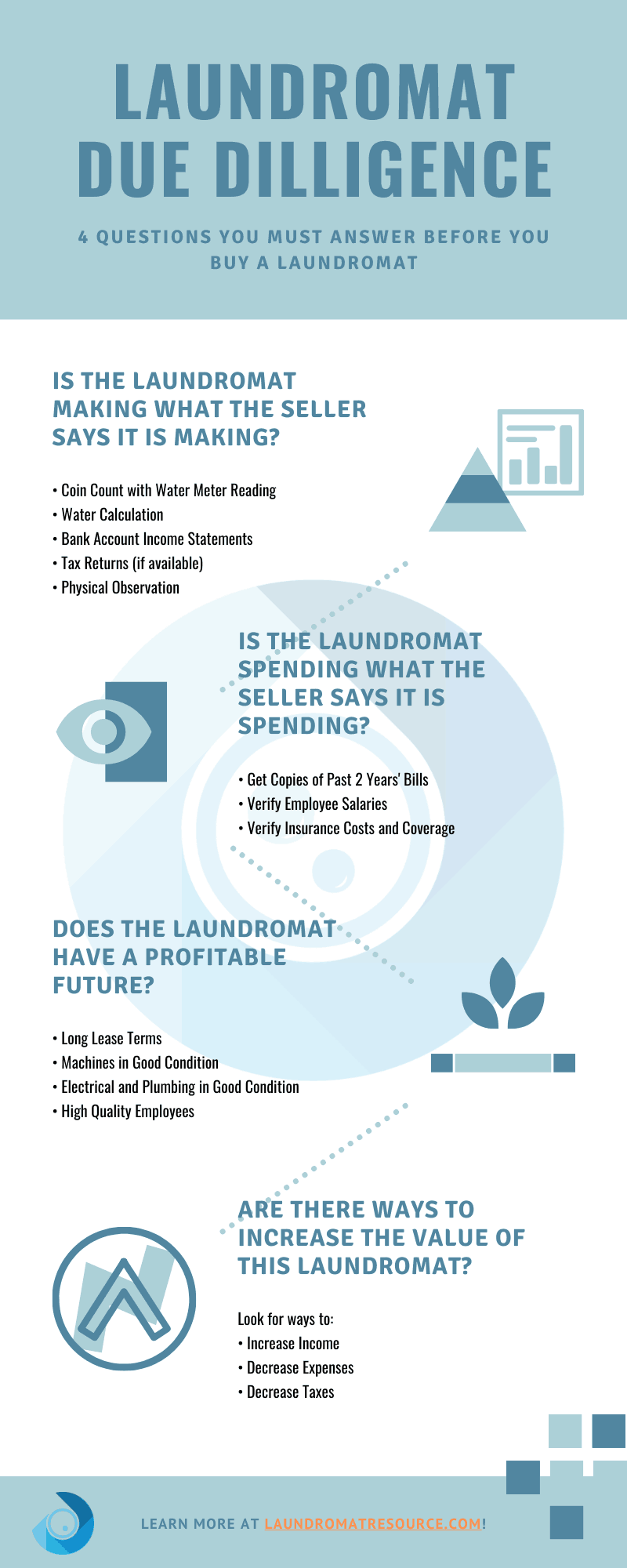

2. Escrow Ensures All Liabilities Are Cleared Before You Take Ownership

Why it Matters:

As a buyer, it’s surprisingly easy to inherit tax debts, unpaid loans, or property liens from the previous owner. Escrow companies research and clear all these to prevent nasty surprises.

Practical Application:

If you’re buying, make sure your escrow team verifies the seller’s sources of financing (like SBA, EIDL, or equipment loans) and pays off any remaining debts (Justin Suh elaborates on this complexity at 31:18). This applies especially to unpaid property taxes, sales tax from vending machines, and employment tax. As a seller, prepare documentation showing your paid-up status and work proactively with your escrow agent to resolve any flags before the sale.

3. Have Your Financing and Documentation Ready BEFORE You Start Escrow

Why it Matters:

Deals often collapse because buyers aren’t financially prepared, or sellers lack crucial documentation. Escrow can’t do its job if the basics aren’t in place.

Practical Application:

Buyers: Line up funding and secure landlord approval as early as possible. If you need financing, get pre-approved. If you’re going solo (no agent), establish a strong, communicative relationship with the seller and landlord (Justin Suh stresses this at 36:44).

Sellers: Have your business license, tax bills, and bank information organized before listing your laundromat. If the business is under an LLC or entity, make sure your escrow disbursement matches your account details.

4. Work With an Experienced Broker or Agent Specializing in Laundromats

Why it Matters:

Business transactions (bulk sale) are much more complicated than typical real estate deals. Specialized brokers know the clauses, contingencies, and protections you need.

Practical Application:

Choose a broker who’s experienced with laundromat sales, not just general real estate (Justin Suh warns against underqualified agents at 16:33). A good broker will help draft agreements, negotiate leases, and insert contingencies to shield you from costly surprises. Remember, saving upfront commission might cost you more in the long run.

5. Understand the Nuances of Bulk Sale (Business Transaction) vs Real Estate

Why it Matters:

Buying the assets of a laundromat (bulk sale) is different than buying the physical property. The liabilities and paperwork involved require special escrow procedures.

Practical Application:

If you’re buying, structure your offer as an “asset purchase” and include language that allows you to assign the contract to your new LLC or corporation (Jordan Berry recommends this at 28:39). Wait to establish your entity until you’re deeper in the process to avoid unnecessary fees if a deal falls through.

6. Keep the Lease Front and Center in Your Transaction

Why it Matters:

The lease is often the biggest reason deals fall out of escrow—if you can’t get a favorable term, walk away.

Practical Application:

Buyers: Secure a lease extension that lets you recoup your investment (typically 5–7 years or longer, depending on the price and equipment age).

Sellers: Facilitate this process by collaborating with the landlord and ensuring there are no unresolved disputes or missing paperwork (Justin Suh addresses this at 47:04).

7. Ask Questions, Be Proactive, and Lean on Trusted Experts

Why it Matters:

Escrow and business purchases can feel overwhelming, but transparency and curiosity cut through confusion.

Practical Application:

Don’t hesitate to ask your escrow officer or broker about any part of the transaction you don’t understand (Justin Suh says they’re always an open book at 51:33). Bring up any concerns early—even those that feel “small,” as they might affect your closing or business future.

Recap & Action Steps

Choose your escrow company and broker wisely.

Get your finances and documents in order before signing agreements.

Clarify and negotiate your lease term as early as possible.

Ask all your questions—never leave your understanding up to guesswork.

Don’t take shortcuts; the right expert saves you time, money, and headaches.

Thinking about buying a laundromat, or prepping to sell yours? Listen to Podcast Show 241 for a deeper dive, and reach out to trusted escrow professionals like Justin at New Century Escrow for personalized advice.

Remember: Knowledge only pays off when you put it into action. Pick one tip above, and take steps this week!

{kind=link}