How Many Laundromats Do You Need to Retire? Key Tips and Practical Steps for Buyers and Owners

Are you dreaming of financial independence with laundromat ownership? You’re not alone. Many believe that owning several laundromats is the ticket to retiring early and living a stress-free life. But how many laundromats do you actually need to retire? In this guide, we break down the main takeaways from Jordan Berry’s expert advice on the Laundromat Resource podcast. Whether you’re considering your first purchase or strategizing as a multi-store owner, these tips are designed to keep your goals grounded in reality and maximize your success.

1. Define Your Personal Financial Independence Number

Tip: Don’t copy someone else’s target—calculate the annual income you need from your laundromats to cover your own lifestyle and expenses.

Practical Application:

Pull bank and credit card statements from the past year. Carefully add up all your core expenses and desired extras. Be brutally honest and factor in a safety buffer. For some, this “lean FI” number might just cover rent, utilities, and basic needs; for others, “fat FI” could include travel, hobbies, and lifestyle upgrades. By choosing your realistic annual number (e.g., $50,000 for lean FI, $100,000 for normal FI, $150,000 for fat FI), you set a concrete target for your investing journey.

2. Know the Formula: Income Needed x Industry Multiple = Required Laundromat Value

Tip: Multiply your annual FI number by the standard industry multiple (usually 4.5–5.5x NOI) to determine the total value of laundromats you need.

Practical Application:

If your financial independence number is $50,000 and the industry multiple is 5x, then $50,000 x 5 = $250,000. This means you’ll need laundromats (single or multiple) with a combined net operating income (NOI) value of $250,000 to reach your goal. Use this formula to reverse engineer your acquisition plan.

3. Don’t Fall Into the ‘Empire Trap’—Quality Beats Quantity

Tip: Focus on buying fewer, higher-performing laundromats instead of chasing an impressive store count.

Practical Application:

Overextending by buying too many laundromats can turn your dream of freedom into a stressful second job. Analyze every purchase through the lens of NOI, efficiency, and scalability. One or two strong locations are often enough to reach most people’s retirement goals. Don’t get distracted by “store count” hype.

4. Factor in Loans and Leverage Wisely

Tip: Your true cash flow is net operating income minus loan payments—plan accordingly if you use financing.

Practical Application:

If your laundromat’s NOI is $50,000 but you have $25,000 in annual loan payments, only $25,000 is left to fund your lifestyle. To accelerate your path, use leverage to acquire more assets, but have a plan for eventually paying down those loans and entering the “harvest” phase where your cash flow (and freedom) increases.

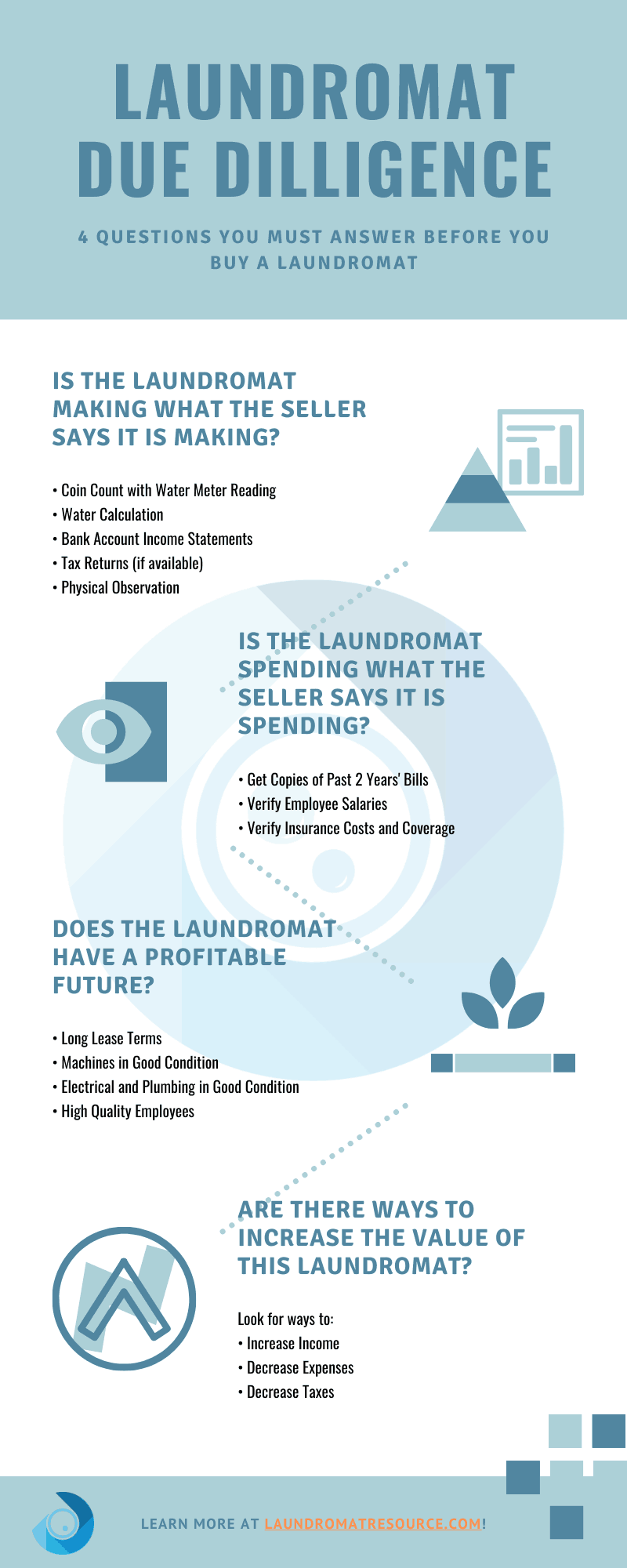

5. Run the Numbers Using Today’s Real Operating Costs

Tip: Use current, not outdated or overly optimistic, numbers when analyzing deals.

Practical Application:

Escape from the “pro forma” trap—request utility bills, rent details, repair histories, and insurance information directly from current owners or records. Test your assumptions: How would your NOI change if utilities spike 20%? Always build in a buffer to reduce the risk of falling short of your FI number.

6. Bigger, Well-Run Stores Usually Outperform Many Small Ones

Tip: Whenever possible, prioritize larger, more efficient laundromats over a scattered collection of smaller stores.

Practical Application:

A few larger locations will streamline management, attract better staff, and spread fixed costs across higher revenue. From both an operations and lifestyle standpoint, owning three strong stores beats managing eight mediocre ones every time.

7. Accept the Reality—Laundromats Are Not 100% Passive

Tip: While laundromats can be highly time-flexible, expect to put in strategic effort and problem-solving.

Practical Application:

Set up strong systems, reliable staff, and embrace new technology to minimize hands-on time. Compare the hours and flexibility required to the grind of a W2 job—laundromat ownership is much more “passive,” but not completely hands-off.

8. Be Strategic About Location—Remote Ownership Is Possible, but Demanding

Tip: You can own laundromats in other markets if you use the right technology and find reliable on-site management.

Practical Application:

In high-cost or highly competitive areas, consider looking outside your local market, but only if you have both a tech stack for remote monitoring and a trusted manager on-site. Never attempt remote operations alone on your first laundromat—seek mentorship or partner locally.

9. Always Transition from Building to Harvesting Assets

Tip: Don’t stay in “builder mode” forever—know when to pay down loans, consolidate, and enjoy your cash flow.

Practical Application:

Monitor your progress, and once your store(s) reach your predetermined FI number, shift focus from aggressive expansion to debt reduction and streamlining. Too many owners burn out by never transitioning from building assets to harvesting their rewards.

10. Leverage Expert Guidance and Community Resources

Tip: Don’t go it alone, especially for your first acquisition—consult industry resources and experienced pros.

Practical Application:

Visit laundromatresource.com for free courses, downloadable resources, or even book a coaching call. Mistakes in due diligence or valuation can cost six figures; a small investment in learning or consulting can save your financial future.

Final Thought

Your path to financial independence with laundromats is unique to your life, your goals, and your market. Start with a clear target, run the real numbers, and focus on quality over quantity. With these actionable tips, you can confidently chart your course toward retirement, one well-chosen laundromat at a time.

Ready to dive deeper or need help running the numbers? Check out the resources at Laundromat Resource and join a community dedicated to helping buyers and owners succeed.

{kind=link}